Read this article in French German Italian Portuguese Spanish

Trendlines: 2023 a peak year for construction equipment sales

28 February 2024

A look at how the year’s unexpectedly buoyant construction market influenced equipment sales

Source: Off-Highway Research

Source: Off-Highway Research

At the start of the year, Trendlines looked at how some expected and unexpected factors added up to a surprisingly buoyant U.S. construction market in 2023. The CHIPS act stimulated some huge factory construction projects, housebuilding stayed resilient despite rising interest rates and infrastructure construction started to tick upwards.

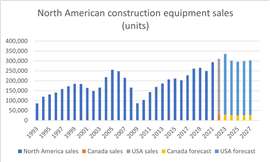

As I write this, Off-Highway Research is finalizing its data on construction equipment sales last year, and the results reflect the strong underlying drivers. Preliminary results suggest sales were up 8% in 2023 to take the market to over 305,000 units sold. It was the third consecutive record year for construction equipment sales and the first time ever that more than 300,000 construction machines were sold in the U.S.

This was all very much at odds with markets elsewhere in the world, most of which fell back slightly in 2023 from the very high levels that were achieved the previous year. For example, equipment sales in Canada dropped around 5% in 2023 and the European market was down by a similar amount.

Top performers

In the U.S., the growth was robust and most of the individual product categories saw increased sales. There were no declines in sales for any machine types – the “weak” performers just stayed at the same high levels achieved in 2022.

Compact track loader sales saw a 5% increase in 2023, with dozers up by more than 8%. (Photo: KHL Staff)

Compact track loader sales saw a 5% increase in 2023, with dozers up by more than 8%. (Photo: KHL Staff)

Among the high-volume products, sales of compact track loaders and mini excavators both edged up by around 5% each, taking both to record volumes. There was even growth in skid-steer loader sales, a product that has been in long-term decline due to their replacement by compact track loaders.

The generally lower growth in compact equipment sales was due to the housing market cooling from the very high levels of activity seen up until interest rates started to rise last year. However, there is still a housing shortage in the U.S., and the industry is robust because of this.

More substantial growth was seen in the heavier equipment categories associated with infrastructure and large-scale nonresidential building work. Sales of graders and dozers were up by significantly more than the 8% market average, as was the articulated dump truck (ADT) market. Such was the popularity of ADTs in the U.S. last year that it accounted for comfortably more than half of global demand for this type of hauler.

But the standout in terms of both growth and volume was the telehandler, with sales rising by around a third in 2023 to take the market over 30,000 machines sold. The versatility of these machines and their application across both residential and nonresidential building put them in the sweet spot for growth last year.

Chris Sleight is the managing director of Off-Highway Research, a market research and forecasting business specializing in analysis of the global construction and agricultural equipment markets.

Chris Sleight is the managing director of Off-Highway Research, a market research and forecasting business specializing in analysis of the global construction and agricultural equipment markets.

Down but not out

It seems inevitable that 2023 will be the high-tide mark for the U.S. equipment market for this cycle. A fall of around 10% in sales is likely this year, to take the market back down to the kind of volumes which were seen in 2021 and 2022. The one-off drivers which elevated sales last year are burning out, particularly for compact and mid-sized equipment, and business confidence might fall as the election draws near due to all the uncertainty that entails.

Objectively, the market will still be good this year. We will most likely see the second or third largest volume of equipment ever sold. Off-Highway Research views it as a return to normal, sustainable levels after the post-pandemic boom. There are no fundamental problems with the drivers of equipment demand. We are simply in the slowdown stage of a cyclical business.

POWER SOURCING GUIDE

The trusted reference and buyer’s guide for 83 years

The original “desktop search engine,” guiding nearly 10,000 users in more than 90 countries it is the primary reference for specifications and details on all the components that go into engine systems.

Visit Now

STAY CONNECTED

Receive the information you need when you need it through our world-leading magazines, newsletters and daily briefings.

CONNECT WITH THE TEAM