Read this article in Français Deutsch Italiano Português Español

2024 Class 8 forecast edges upward

29 February 2024

ACT Research has revised its 2024 Class 8 production and sales expectations upward in its latest North American Commercial Vehicle Outlook. The revision comes on the heels of unexpectedly strong Class 8 net orders in January.

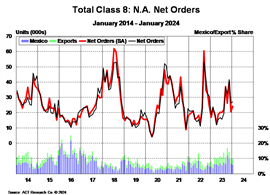

According to the latest State of the Industry: NA Classes 5-8 report, January Class 8 net orders were up 45% year over year to 27,125 units. Total Classes 5-7 orders also rose by 14% y/y to 19,954 units.

“U.S. Class 8 tractor orders surprised to an above-replacement level of 16,765 units, up 44% y/y,” said Kenny Vieth, ACT’s president and senior analyst. “Seasonality is one component but given the state of for-hire truckload rates, we continue to suspect private fleets as the primary driver behind U.S. tractor demand. As well, the LTL (Less-Than-Truckload) segment remains a bright spot relative to TL and is likely also contributing.”

At ACT Research’s semi-annual seminar hosted in February, Bill Kretsinger, chairman and CEO at American Central Transport, Joe Vitiritto, president and CEO at PAM Transport, and Marshall Franklin, CEO and CFO at Highway Transport, seemed to corroborate the increase in demand. When asked about equipment purchases, they all shared that fleets generally didn’t get the allocation they expected during the pandemic, and now it’s time to catch up, with fleets right sizing now and getting back to a regular trade cycle, ACT reported.

Industry leaders said fleets didn’t get the allocation expected during the pandemic and “now it’s time to catch up.” (Photo: KHL Staff)

Industry leaders said fleets didn’t get the allocation expected during the pandemic and “now it’s time to catch up.” (Photo: KHL Staff)

“It’s currently a very mixed market,” Veith acknowledged. “On one hand, we have a very weak situation in the U.S. for-hire tractor market as significant 2023 private fleet share gains took loads out of an already weak 2023 freight market. On the other, there is lingering pent-up vocational truck demand in the U.S. and Canada, a reshoring- and peso-fueled resurgence in demand for equipment in Mexico, and a still-healthy U.S. macroeconomic story bolstered by a swing in the retail inventory cycle from the destocking that occurred through 2023.”

He noted that the decision to boost the forecast, despite near-term inventory risks, “reflects the industry’s ability to more aggressively sell into Mexico and export markets, while maintaining strength in domestic vocational. The 2024 market is atypically bifurcated: considerable strength remaining in U.S. and Canadian vocational markets and Mexico helps offset otherwise weak demand in U.S. and Canadian tractor markets, LTL excluded.”

Mexico-bound Class 8 production is expected to rise considerably in 2024, due to more time-sensitive manufacturing loads to transport, pent-up demand and a strong peso.

Regarding the 2024 U.S. economic outlook, David Teolis, ACT Research’s Chief Economist, in a seminar presentation, pointed out, “Economic developments that will affect 2024 are interest rate cuts, wage inflation, elections, supply chain and worker shortage. ACT’s economic outlook is for a gradual slowdown through mid-2024, then an upward tick through 2025.”

Veith believes “the economy’s cooperation, plus the OEMs’ desire to ensure supply-chain integrity by making sure the industry’s labor supply remains largely intact through 2024, adds upside to our higher forecast.”

However, he added a cautionary note, “While we view upside as more likely than down,” he said, “we remain concerned that the largest piece of the North American market, U.S. for-hire truckload, is unlikely to be helpful in driving volume this year.”

Brought To You By

|

POWER SOURCING GUIDE

The trusted reference and buyer’s guide for 83 years

The original “desktop search engine,” guiding nearly 10,000 users in more than 90 countries it is the primary reference for specifications and details on all the components that go into engine systems.

Visit Now

STAY CONNECTED

Receive the information you need when you need it through our world-leading magazines, newsletters and daily briefings.

CONNECT WITH THE TEAM