Read this article in Français Deutsch Italiano Português Español

ACT Research: March Class 8 orders decline, April forecast remains unchanged

30 April 2024

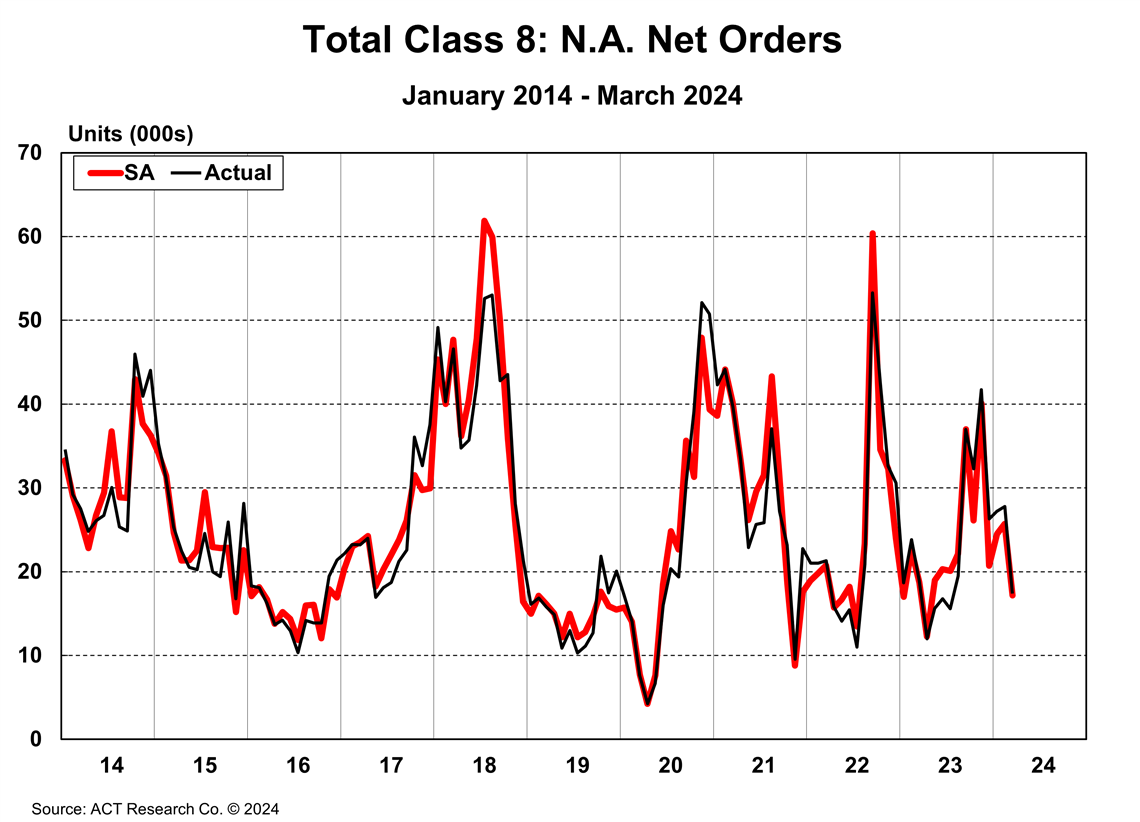

In its latest “State of the Industry: NA Classes 5-8” report, ACT Research reported that final March Class 8 net orders totaled 17,410 units (17.2 thousand seasonally adjusted) — a decline of 8.4 percent year-over-year. Kenny Vieth, president and senior analyst for ACT, said this may signal a slowdown in capacity additions, “a requisite for the freight market to turn after a year of growth that defied typical fundamentals.”

Graph: ACT Research

Graph: ACT Research

Vieth added because the second and third quarters are typically the weakest of the year for orders, “the call is not prescient.”

U.S. tractor orders in March were down 1.3 percent year-over-year to 10,400 units, ACT Research said. In the vocational market in March, total North American Class 8 truck orders dropped 2.0 percent year-over-year to 5,300 units.

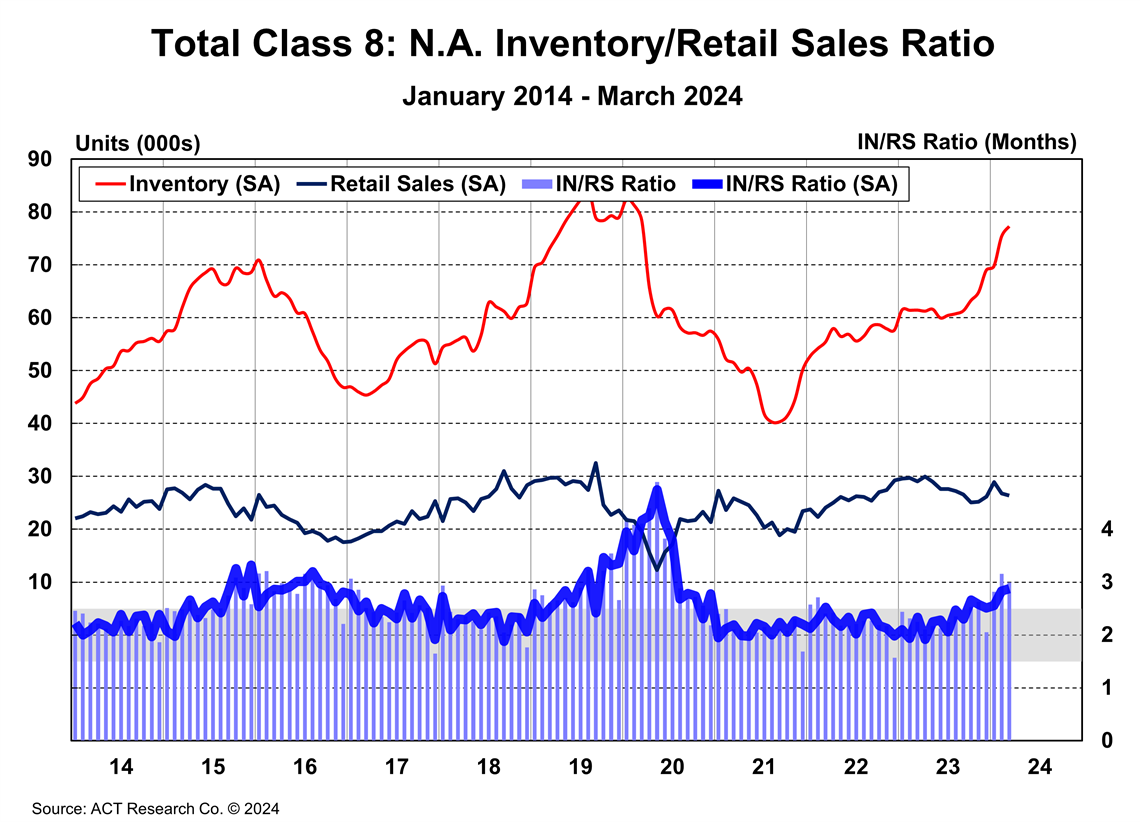

“Between strong production and softening U.S. tractor sales the past six months, Class 8 inventories have risen substantively,” Vieth said. “Since last September, Class 8 inventories have risen nearly 15,000 units, hitting another four-year high in March.”

Vieth added that Class 8 build totaled 29,854 units in March, down 5 percent year-over-year, but said the Easter holiday meant three fewer production days. Total Class 8 retail sales in March were down 13 percent year-over-year to 25,942 units, he said.

For Classes 5-7 in March, total orders rose 23 percent year-over-year to 25,359 units (23.4 thousand seasonally adjusted).

Graph: ACT Research

Graph: ACT Research

“Classes 5-7 inventories remained highly elevated in March, as medium-duty bodybuilder labor and supply-chain challenges persist,” Vieth said. “Inventory totaled 89,360 units on a nominal basis, up 22 percent year-over-year. Retail sales remained healthy at 20,320 units.”

April Forecast Unchanged

Regarding its Class 8 forecast, ACT Research said in a recent press release that its April forecast would remain essentially unchanged from what the organization published in its latest North American commercial vehicle forecast. This follows “pushing up” its original forecasts for February and March, ACT said. Vieth said this was due to indicators in March of cooling demand coupled with traditionally weak orders in the second and third quarters of the year.

“With spot rates still at sharp operating loss levels into early April and carrier profitability halved in the past two years, we continue to pose the question: who’s buying Class 8 tractors at the bottom of the cycle?” Vieth said. “Certainly, it is not embattled for-hire TL fleets. Our answer over the past year has been private fleets, who have reclaimed freight from load boards and taken market share from for-hire markets.”

He said that while ACT Research expected the sharp contraction in for-hire carrier profits to rebalance the market in 2024, what has instead happened is that private fleets have begun heeding OEMs’ cautions about costs ahead of the U.S. Environmental Protection Agency’s (EPA) Clean Trucks emissions regulation, which becomes effective with the 2027 model year.

“Current estimates are putting the day one cost of the mandate, inclusive of taxes, at around $30,000 per Class 8 unit,” Vieth said. “Most of that added cost is tied to the warranty and useful life extensions. With around 40 percent of Class 8 buyers purchasing warranty extensions due to high-mileage operations (for-hire TL), not all carriers will feel the regulation’s bite equally.”

Vieth added, “Given the anticipated pre-EPA 2027 mandate demand swell into 2026, supply chain integrity is an especially critical commercial vehicle activity in 2027. Private fleet capacity positioning is just one part of the ‘this purchasing cycle is different’ story along with ongoing domestic vocational and Mexico market strength.”

POWER SOURCING GUIDE

The trusted reference and buyer’s guide for 83 years

The original “desktop search engine,” guiding nearly 10,000 users in more than 90 countries it is the primary reference for specifications and details on all the components that go into engine systems.

Visit Now

STAY CONNECTED

Receive the information you need when you need it through our world-leading magazines, newsletters and daily briefings.

CONNECT WITH THE TEAM